As SpaceX prepares for the largest IPO in history, the more investable story may be the hardware ecosystem it cannot build without — and the Asian manufacturers quietly at the center of it.

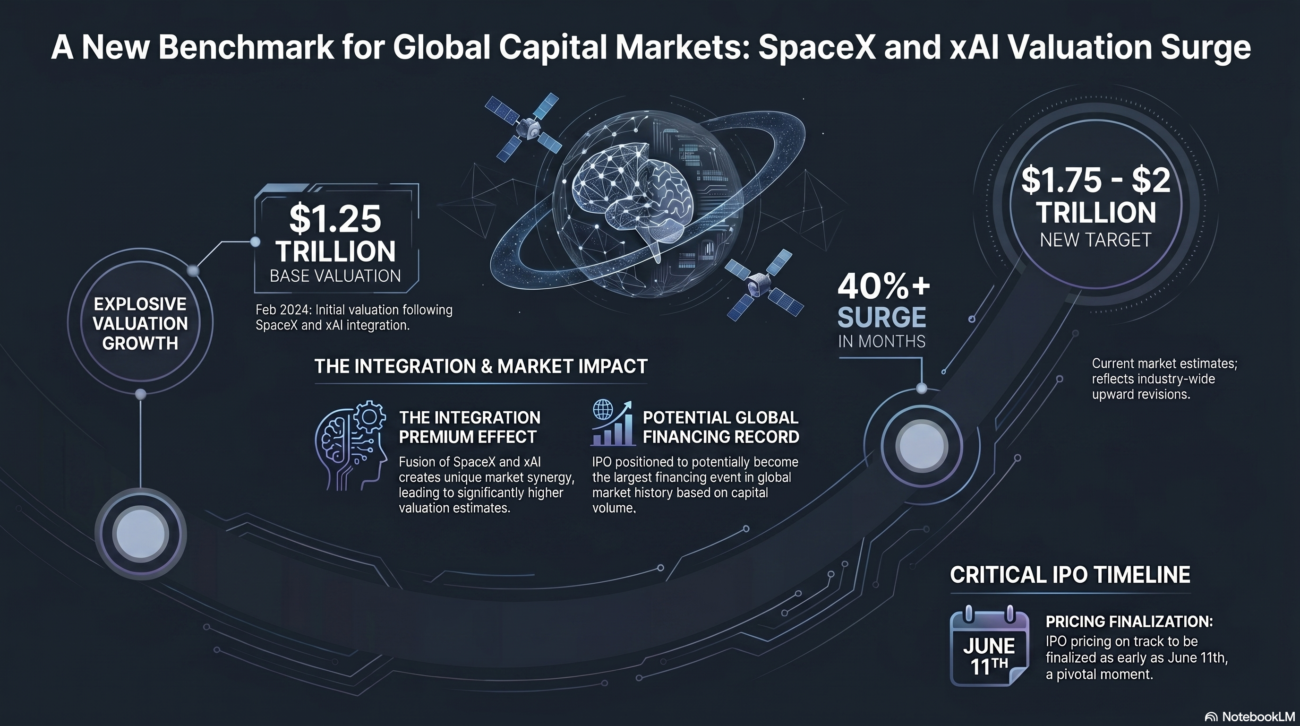

On April 1, 2026, SpaceX filed a confidential draft registration statement with the U.S. Securities and Exchange Commission. The company is targeting a June 12 listing on the Nasdaq under the ticker SPCX, with an offering expected to raise up to $75 billion at a $1.75 trillion valuation — more than double the previous record set by Saudi Aramco in 2019.

SpaceX is no longer simply a rocket company. The February 2026 all-stock merger with xAI created a combined entity spanning launch services, satellite internet, and artificial intelligence. At $1.75 trillion, public investors are being asked to price a vertical integration thesis that has never previously existed in a single listed company.

The financial foundation is Starlink. The service crossed 10 million subscribers in February 2026, generating approximately $11.4 billion in revenue in 2025 with a 63% EBITDA margin. Starlink is adding an estimated 1.5 million new subscribers monthly in 2026, with projected revenue of $15–20 billion by year-end. It constitutes roughly 65% of all active satellites in low-Earth orbit globally.

The valuation math, however, demands scrutiny. At 87–116x 2025 revenue, SpaceX is priced for a future that requires flawless execution across three distinct businesses simultaneously — one of which, xAI, posted a $6.4 billion operating loss in its first year as part of the group.

The Angle the Market Is Missing

Most coverage of the SpaceX IPO is focused on the obvious variables: Musk, Starlink subscriber counts, the dual-class share structure, and whether $1.75 trillion is defensible. These are reasonable questions. They are also the questions every institutional investor is already asking.

The more productive line of inquiry runs upstream: who builds the hardware that makes Starlink work? Each Starlink subscriber requires a user terminal — a precision-engineered ground device containing RF modules, high-density printed circuit boards, ceramic substrates, and antenna arrays. At 10 million subscribers and growing, the production volume required is substantial. At 1.5 million new users per month, that terminal demand is structural, not episodic.

Taiwan’s electronics manufacturing sector sits at the center of this supply chain. Approximately 50 Taiwanese companies produce sensitive components and ground equipment for the Starlink ecosystem. SpaceX has spent the past 18 months actively directing its Taiwanese suppliers to shift production to Vietnam and Thailand — not because the relationships are changing, but because the geopolitical exposure of concentrating production in Taiwan is no longer acceptable to a U.S. national security contractor.

“The demand from satellite systems for high-precision circuit boards aligns perfectly with the technological advantages of Taiwanese manufacturers.”

— TRADING KEY RESEARCH, MARCH 2026

The supply chain migration creates a two-track opportunity: companies that hold the technology relationships with SpaceX, and companies building new manufacturing capacity in Southeast Asia to service those relationships. Several are publicly listed. Several are small enough that institutional capital has not yet moved meaningfully.